Special Needs Trusts Online Can Help!

I am a Special Needs Trust Attorney and I am here to help. I am the founder of a nonprofit corporation to that provides quality information about resources available to families as well as providing affordable Special Needs Trusts and estate planning for families. I have over 20 years of experience helping families just like yours. Find out more information at SpecialNeedsTrustsOnline.com or click here to set up a free appointment.

I am a Special Needs Trust Attorney and I am here to help. I am the founder of a nonprofit corporation to that provides quality information about resources available to families as well as providing affordable Special Needs Trusts and estate planning for families. I have over 20 years of experience helping families just like yours. Find out more information at SpecialNeedsTrustsOnline.com or click here to set up a free appointment.

Source: specialneedstrustsonline.com

I am Tom Sannicandro, a

I am Tom Sannicandro, a  Store your Wills and Trust safely.

Store your Wills and Trust safely.

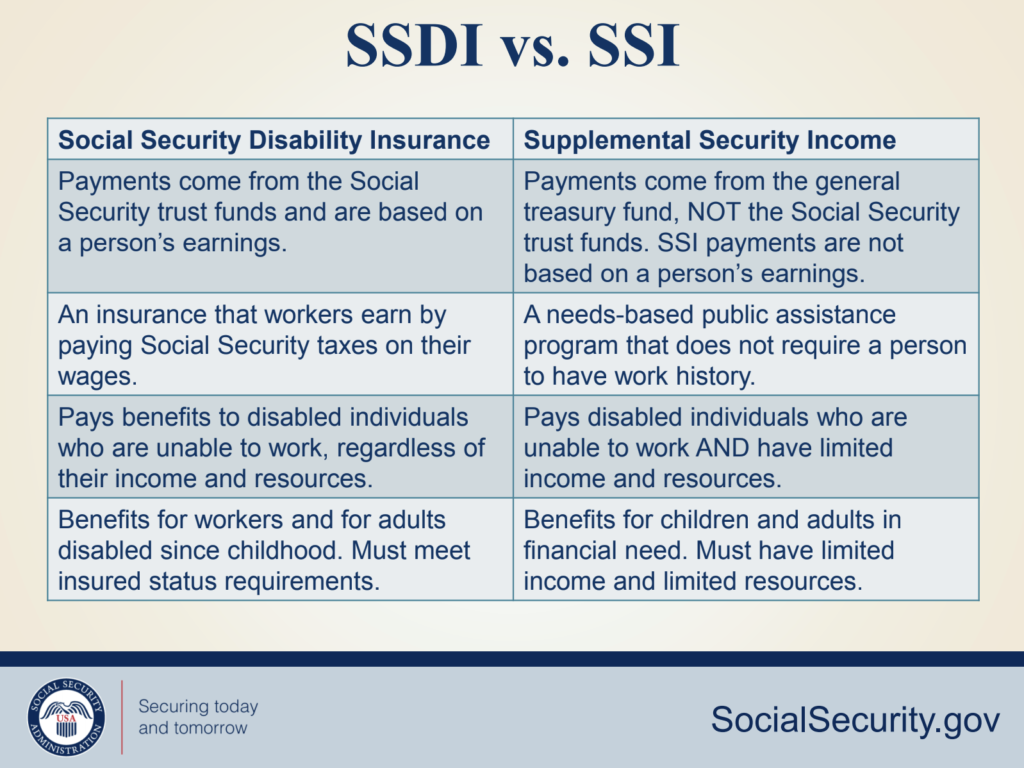

The trust is intended to help preserve funds for a person with a disability, and enhance the person’s quality of life while protecting his or her eligibility for public benefits, such as Medicaid and Supplemental Security Income (also known as “SSI”).

The trust is intended to help preserve funds for a person with a disability, and enhance the person’s quality of life while protecting his or her eligibility for public benefits, such as Medicaid and Supplemental Security Income (also known as “SSI”).